Word on the High Street – Retail Trends and Strategies

LFRA members heard from Jacqueline Windsor, Partner – Retail Strategy, PwC UK on its recent Overseas Study Tour about global retail trends and how brands adapted to the everchanging customer needs and economic circumstances.

Below are some key insights LFRA learnt from Ms Windsor’s presentation.

Consumer spending habits

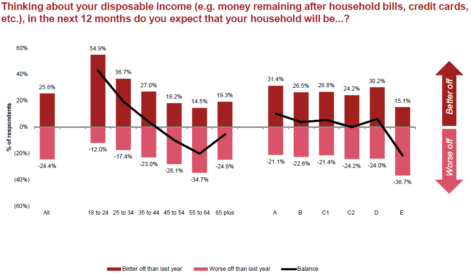

PwC discovered in its recent Consumer Sentiment Survey (April 2019) that consumer confidence is resilient despite political and economic conditions, with younger people (18-34 years) more optimistic about their disposable income.

They believe they will be better off over the next 12 months compared to 45-65+.

Source: PwC Consumer Sentiment Survey April 2019 (n=2,074)

“Younger people are always more optimistic, because they haven’t lived through a recession and are increasingly living at home, so more money in their pockets to spend on discretionary stuff,” comments Ms Windsor.

Source: PwC Consumer Sentiment Survey April 2019 (n=2,074)

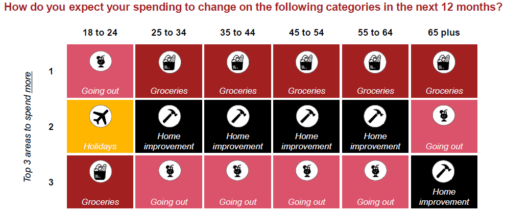

Surprisingly consumer spending priorities of 25-64 year olds are the same, with an expected increase in spending on groceries and other everyday essentials, followed by home improvement and going out/leisure.

“As you can see, groceries are pretty much the number one thing [consumers] are going to spend for profit, but that is not driven by volume, that is driven by expectations of higher prices,” explains Ms Windsor.

An expected increased spending on home improvement is a positive indication for Large Format Retailers as many specialise in home improvement, furniture, lighting, white goods, bedding.

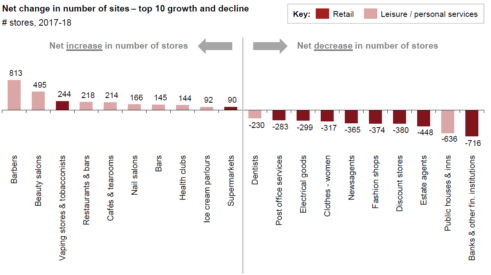

This research also reflects tenancies in successful Australian homemaker centres, where Large Format Retail stores are mixed with supermarkets, leisure and everyday essentials like chemists and food outlets. The graph below supports this tenant mix, highlighting a remarkable increase in the number of leisure/personal services sites.

Source: LDC

Source: PwC Consumer Sentiment Survey April 2019 (n=2,074)

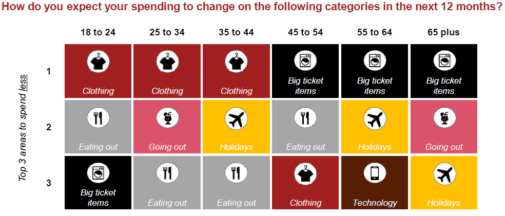

Conversely, the main priority for spending cut back for 18-44 year olds is clothing, whereas 45-65+ expect to decrease spending on big ticket items like furniture and whitegoods.

Spending less does not necessarily equate to cutting out but rather buying less or finding a better deal. Big ticket items are likely to be a necessity for 18-44 year olds as they tend to be renters, first homebuyers or renovating to accommodate a growing family. Whereas the 45-65+ age group are most likely to be homeowners who are more practical and do not feel the need to replace existing big ticket items.

Source: Barclaycard Consumer Spending Report (Q4 2018)

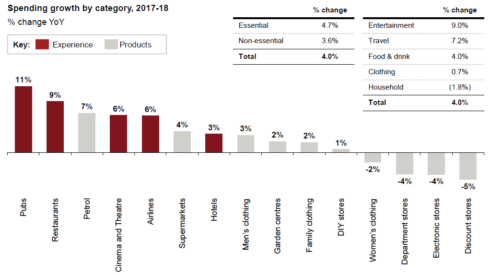

Ms Windsor also explained that there is a consumer trend to spend more on experiences, particularly amongst millennials. This is demonstrated in the above graph with spending growth at pubs, restaurants, cinemas and travel.

It is evident that consumers are spending more on experiences than material items. This finding informs Large Format Retailers that there is a need to transform product and service offerings, to provide more experience-based services and to be creative with their customer service and engagement.

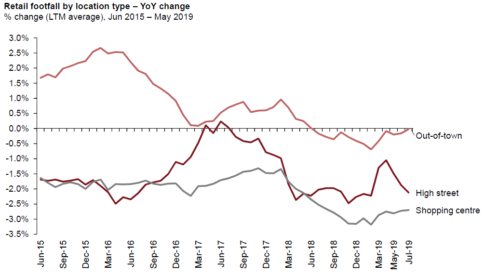

Retail footfall trends

Source: BRC

There has been a downward trend in retail footfall over the past four years. Although there has been less foot traffic, this graph does not consider the quality of the time spent at the store. It does not reflect whether there has been stabilised or increased likelihood of sales. The decrease in retail footfall may be explained by consumers being time-poor and not having time to browse or go ‘window-shopping’, with consumers more likely to have an intention to visit a store to purchase.

Ms Windsor explained out-of-town retail (Large Format Retail) being more resilient than high street for multiple reasons. They include parking availability, size allowing experiences to be created instore, and consumers likely to research, ask questions and educate themselves on products before committing to a big ticket item purchase.

Online disruptors

Online disruption is happening in almost every consumer-facing industry, with online providers competing with established ‘real world’ brands for market share. Notable examples include Blockbuster and Netflix, San Disk and Dropbox, Telefonica and Skype, and Accor Hotels and Airbnb.

With the emergence and success of online disruptors, Ms Windsor explains that retailers need to be proactive and innovative to attract consumers.

“There are five levers retailers are pulling to try to compete against the online disrupters; newness (a reason to visit the store), redefining the role of the store, retail logistics, technology solutions, and collaborations and partnerships,” outlined Ms Windsor.

Newness and redefining the role of the store is evident in H&M’s sustainability initiative Take Care which includes an in-store repair station for worn H&M clothes, garment-care products as well as online advice about care, repair and recycling unwanted garments.

Technology solutions include initiatives where retailers incorporate technology for increased efficiency but still maintain the human desire to socialise. Collaborations and partnerships go beyond celebrity-endorsed products and include business partnerships to increase customer reach and sales, like retailers offering Afterpay or Zip Pay as an alternative online payment option.

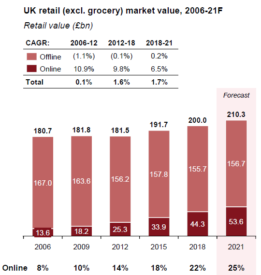

Source: GlobalData

Overall UK retail market value has grown, with the online market value significantly contributing to this growth. Despite fears of physical retail demise and store closures, offline retail market value has been steady post-GFC. It can be argued that online retail complements brick and mortar retail and does not undermine it.

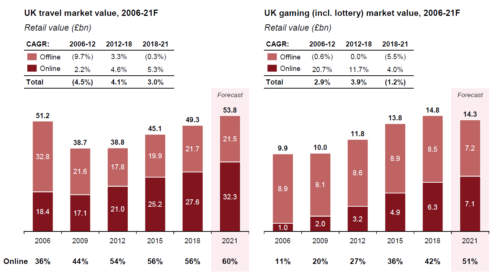

Source: PhocusWright, H2G

This is also evident in industries such as travel and gaming where an online presence extends service and accessibility. For example, Flight Centre has both an online and physical store presence in Australia, with each platform providing a different service. Flight Centre’s online website and app provide travellers the option to search, compare and book online instantly. Instore offers a consultation service where customers can ask questions about their travel plans.

Despite the increasing online trend, physical retail stores are still relevant for a variety of reasons.

Brick and mortar is essential

Retail stores fulfil four main criteria for customers that online channels are unable to satisfy:

- Experience the product in person (i.e. to see/touch/test products). This helps customers feel more confident in comparing features that are difficult to assess online

- Have a human connection, whether customers are looking for technical content and information or reassurance

- Provide assurance there is a physical location customers can go to if there are any issues with their purchase. Many believe staff at a store will resolve problems quicker than online bots or assistants

- Select, transact and deliver faster, particularly when speed is an important criteria for customers (e.g. replacing broken appliance)

These factors are particularly important in providing additional reassurance when shopping for big ticket and technically complex products, which are usually sold in Large Format Retail stores and homemaker centres.

Big ticket and technical items tend to be relatively costly infrequent purchases. Considering this significant financial investment, consumers actively seek assistance, advice and assurance from retailers given their limited knowledge or familiarity with the product.

Consumers may browse online to narrow down options but will eventually visit a store when they are ready to commit to a purchase. This explains the relatively resilient retail footfall at Large Format Retail sites addressed earlier in this article.

“I don’t think online per se will take away from the store, but the store can’t think of itself as a single channel”, said Ms Windsor.

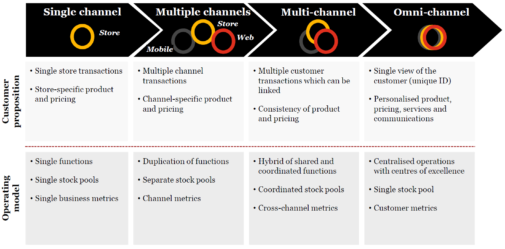

From single channel to omnichannel

To survive in today’s market, retailers cannot be single channel (physical store-only). There is a need for many channels to service different needs and offer different access points and solutions.

Recently there has been a movement towards omnichannel for a seamless customer experience no matter which channel, whether it is online or instore, they choose to interact with the brand.

Source: PwC

Ms Windsor recognises that for retailers to shift from multi-channel to omnichannel, a complete redesign of the business is required.

“If the business is organised to serve channels and not customers, it’s hard to create those incentives across the group.”

Retailers are encouraged to dismantle earlier beliefs that each channel is a separate division in retail and grasp the concept of a frictionless and holistic customer experience. For example, if a product is not available instore then staff can instantly order the product online for the customer and have it delivered to their door.

Because it is frictionless, each channel is expected to provide customers the same range of products and/or services with no difference in range, price and convenience.

Additional shifts in retail

Retail has transformed to adapt to changing markets and customer needs. Ms Windsor concludes the presentation by highlighting and summarising the following shifts.

Consumer push –> Consumer pull

In the past brands created products and pursued consumers and pushed them to buy, whereas now it is almost reversed. Products are created based on what customers want. Information can be gathered through customer feedback, market research, or observing emerging styles and trends.

Static collections –> Dynamic collections

Having a dynamic collection is ‘newness’ and gives people a reason to visit. Seasonal collections are an example of how retailers can easily add or modify their stock to attract existing and/or new customers.

Mass broadcasting –> Personalised engagement

Consumers are more likely to respond to personalised communication than mass communication. Personalised engagement could be as simple as recording email addresses and personalising newsletters with a customer’s name, or creating personalised correspondence by learning about the customer based on previous transactions and other interactions. Another method of personalised engagement is using targeted online advertisements created from extensive market research and web browser tracking.

E-commerce –> Social commerce

E-commerce has evolved into social commerce where there is a desire for a more enhanced customer experience. In addition to browsing and purchasing, which was offered in e-commerce, consumers can socialise with the brand by commenting in the ratings section, interacting with the brand on social media, or promote a brand’s initiative or ethos.

International and national –> Local

Ms Windsor explained that there has been a reversal in the trend where years ago consumers wanted to be global citizens and sought after products from other countries. Now, consumers as humans want to rely and buy from a brand or source they can trust and that tends to be local.

Retailers –> Brand

The focus on brand personification and its social identity allows consumers to connect with and trust the brand and its vision.

Transactional –> Experiential

Interaction between consumers and brands have become more substantial and relationship-based. Brands and homemaker centres are driven to be innovative and create memorable experiences regularly, particularly instore, to attract customers.

Retail sector –> Convergence of sectors

Over time, retail has developed into a multifaceted sector. The convergence of sectors relates to the diverse experts involved in retail collaborating and sharing their knowledge. Experts in logistics, finance, marketing and data scientists have different touch points but are all involved in the same brand or project.

Zero-sum game –> Win-win partnerships

It was previously believed that brands were strictly competitors, sticking to their lane and competing for consumers’ attention and market share. Although that may be true to some extent, partnerships can introduce brands to a wider customer base, expand a brand’s offering and offer something new, a win-win for both parties.

“One of the things you can do is have unique product, and that is collaborations,” said Ms Windsor.

“It could be exclusives and it doesn’t have to be just exclusive collaboration. It could be exclusive skews or products or packaging and the way that people are thinking about it is quite novel.

“Whether that gives you exclusive product, whether that gives you a channel, so there’s lots of things about online players partnering with retailers because it has a physical footprint.”

Conclusion

LFRA Overseas Study Tour members found the meeting with Jacqueline Windsor, Partner – Retail Strategy, PwC UK incredibly insightful and a highlight of the trip.

Ms Windsor’s extensive analysis of retail trends and its effects were practical. Attendees could bring ideas back to Australia and apply them to their businesses. Although some examples used were UK-based, LFRA members were able to relate with those examples in an Australian context.

Overall it is a dynamic time for retail, where innovation, creativity and connectivity are necessary for brands to survive.

This article is a part of a 10-segment series covering the 2019 LFRA Overseas Study Tour.