Payroll Tax – Where You Set Up Your Business May Be More Important Than You Think

When an individual or company decides to set up or expand a business, several factors need to be considered before any significant decisions can be made or executed.

Some of these factors include researching the market, developing a business plan, choosing the appropriate business structure to adopt, understanding the relevant legal obligations that need to be complied with and so on.

With the recent introduction of lower payroll tax rates for regional employers, the location of a business should be a more prominent discussion that is had earlier.

Payroll tax

Payroll tax is a self-assessed state and territory tax which is assessed on wages paid or payable by an employer to its employees. This tax is then calculated on the amount of taxable wages an employer pays each month and is payable in each state or territory of Australia where an employee performs services for an employer.

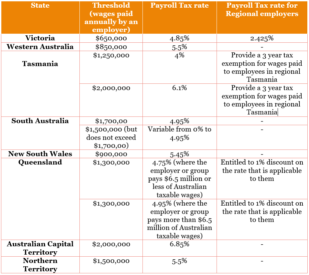

Currently, employers are required to pay payroll tax at the appropriate rate (dependent on the type of employer they are and the amount of taxable wages they pay) where they exceed the following thresholds:

Currently, employers are required to pay payroll tax at the appropriate rate (dependent on the type of employer they are and the amount of taxable wages they pay) where they exceed the following thresholds:

The Victorian and Queensland State Governments have introduced concessional payroll tax rates with the aim to increase employment in regional areas. The concessional payroll tax is only applicable to those considered to be ‘regional employers’ under respective legislation.

This has also been witnessed in Tasmania with the introduction of a three-year payroll tax exemption for wages paid by a business to its employees in regional Tasmania, where an interstate business relocates to Tasmania and establishes its operations in a regional area between 1 July 2018 and 30 June 2021.

In light of these concessions, employers operating in these states or intending to do so in the future should consider if they qualify as a regional employer to ensure they are taking advantage of the lower rates.

Requirements to be considered as a regional employer

As the above table outlines, employers in Victoria, Queensland and Tasmania may be entitled to a concession in the payroll tax rate that is applicable to them where they are considered to be a regional employer.

This requires a company in Queensland:

- To have their principal place of employment in regional Queensland; and

- Have at least 85% of its taxable wages paid to regional employees.

In satisfying these requirements, the principal place of employment will be the company’s registered business address if the company holds an ABN, otherwise it will be the place at which the principal place of business is located.

A regional employee will then be someone whose principal place of residence is in regional Queensland. In determining whether an employee’s principal place of residence is in regional Queensland, the following link will provide assistance in establishing what areas would be considered as regional Queensland: https://itt.abs.gov.au/itt/r.jsp?ABSMaps.

Similarly, a company in Victoria would be required:

- To have their principal place of employment in regional Victoria; and

- Have at least 85% of its taxable wages paid to regional employees.

In establishing whether an employer is primarily based in Victoria, the following link details which areas are in fact considered to be regional Victoria: https://www.sro.vic.gov.au/ptxregional.

However unlike in Queensland, the regional employee ‘definition’ differs. A regional employee is someone who performs more than 50% of their services in regional Victoria during the month.

Furthermore, the Tasmanian payroll tax exemption would be applicable to:

- Eligible businesses who relocate to areas which are not within the local government municipalities of Hobart, Clarence, Glenorchy or Kingborough; and

- Wages paid to employees that conducts at least 80% of their work in regional Tasmania (that being outside of the municipalities outlined above).

Such eligible businesses would include employers who have:

- An existing business in a location other than Tasmania prior to the relocation; and

- Not paid taxable wages in Tasmania (either themselves or as a member of a group) in the 5 year period preceding the relocation; and

- Relocated or expanded its business, in part or entirety, to regional Tasmania; and

- Commenced physical operations from real property in regional Tasmania; and

- Commenced the payment of wages for work conducted in regional Tasmania.

Rebates

The respective State Revenue Offices also have a number of Payroll Tax Rebate Schemes which entitles business to various payroll tax rebates, particularly in relation to apprentices and trainees.

This is currently evident in Tasmania, where a two year rebate scheme exists for businesses that employ apprentices and trainees in the building and construction, tourism and hospitality and manufacturing industries, entitling employers to receive rebates where they meet the relevant requirements.

Additionally, Queensland also entitles businesses to claim a 50% payroll tax rebate on apprentice and trainee wages which are exempt from payroll tax, thereby reducing the payroll tax amount the employer would be obligated to pay for that period.

Key Takeaways

Based on the payroll tax rates that apply in each state and territory, along with the relevant rebates which exist for employers who engage apprentices and trainees, businesses should factor in the potential benefits and consequences of operating and employing individuals in various locations around Australia to ensure educated business decisions are made and unnecessary costs are not incurred.

Considering that the regional payroll tax rate in Victoria will again be reduced from 1 July 2020, to eventually reach the rate of 1.2125% by the 2023 financial year, decisions about operation and location should be a forefront matter.

New opportunities may arise for businesses, particularly as regional areas in various states grow and develop. Even where a business is already operating, consideration of the reduced payroll tax rates for regional employers should not disregarded where there is a possibility that the above requirements could be satisfied.

Anne Bailey, Partner, PwC &

Paula Dolezal, Consultant in Employment Taxes, PwC